IMARC Group has recently released a new research study titled “South Korea Cloud Computing Market Report by Service (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS)), Workload (Application Development and Testing, Analytics and Reporting, Data Storage and Backup, Integration and Orchestration, Resource Management, and Others), Deployment Mode (Public, Private, Hybrid), Organization Size (Large Enterprise, Small and Medium Enterprise), Vertical (BFSI, IT and Telecom, Retail and Consumer Goods, Energy and Utilities, Healthcare, Media and Entertainment, Government and Public Sector, and Others), and Region 2025-2033”, offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and future market scenarios.

South Korea Cloud Computing Market Overview

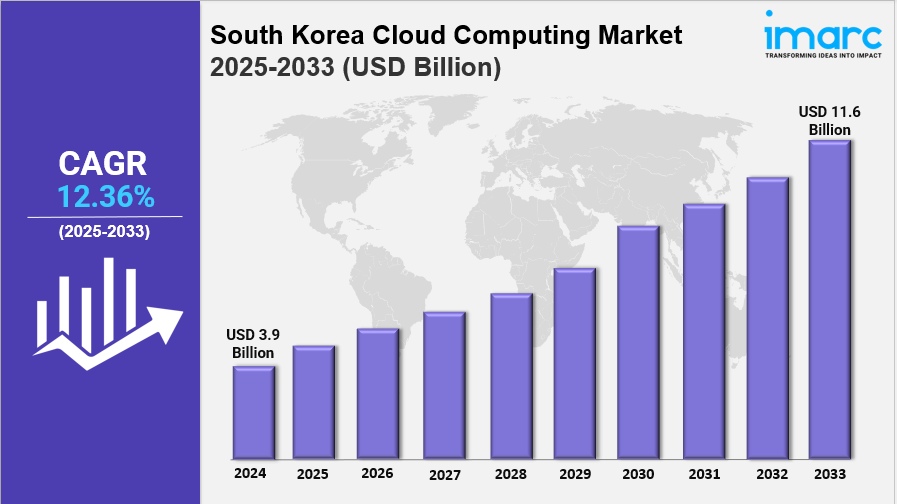

The South Korea cloud computing market size value of USD 3.9 Billion in 2024 and is projected to attain USD 11.6 Billion by 2033, growing at a CAGR of 12.36% during 2025-2033. The market is notably driven by rising cybersecurity concerns, digital education, and healthcare adoption.

Study Assumption Years

- Base Year: 2024

- Historical Year/Period: 2019-2024

- Forecast Year/Period: 2025-2033

South Korea Cloud Computing Market Key Takeaways

- Current Market Size: USD 3.9 Billion (2024)

- CAGR: 12.36% (2025-2033)

- Forecast Period: 2025-2033

- The market is forecast to reach USD 11.6 Billion by 2033.

- Software as a Service (SaaS) holds the largest market share among services.

- Resource management represents the dominant workload segment.

- Public deployment mode is the leading market segment.

- The BFSI sector is the top vertical, and the West region holds regional dominance.

- Key government initiatives and increased investments are spurring adoption across industries.

Sample Request Link: https://www.imarcgroup.com/south-korea-cloud-computing-market/requestsample

Market Growth Factors

The South Korea cloud computing market is primarily driven by increased incidences of cybersecurity threats and data breaches, which have heightened the need for robust security solutions and disaster recovery systems in the country. According to the report, the South Korean Ministry of Science and ICT significantly increased the national budget for cloud computing, planning an investment of US$ 91.5 million in May 2024. Notably, about US$ 18.1 million is allocated for the development and commercialization of cutting-edge cloud services, with another US$ 6.0 million directed toward transforming traditional software into SaaS models. Growing digital threats, such as the North Korean hacking incident in May 2024 where 1,014 gigabytes of sensitive data were stolen from a South Korean court computer system between 2021 and 2023, bolster market demand.

Government policies and digital transformation initiatives also shape market progress. The Ministry of Science and ICT’s ambitious plans aim to bolster the local industry and facilitate the adoption of advanced cloud infrastructure, encouraging both public and private sector collaboration. The government specifically allocated US$ 5.3 million to nurture cloud-based SaaS solutions. Additionally, strategic collaborations in healthcare, finance, and other verticals are fast-tracking cloud adoption, supported by rapid digitalization and remote working trends. Between 2015 and 2021, the number of remote employees surged from 66,000 to 1.1 million, mainly due to the COVID-19 pandemic, showcasing a 17-fold increase that fueled reliance on cloud solutions.

Rapid technological advancement in South Korea contributes further to market expansion. The country ranked 5th globally in the Global Innovation Index in 2021 and held the sixth-largest private investment in artificial intelligence as of 2022. This technological prowess, coupled with increasing integration of big data and machine learning in business operations, has heightened demand for scalable and flexible cloud services. Companies are also responding to the rise in remote work and complexity of operations by leveraging resource management and public cloud platforms, evidenced by recent launches such as the April 2024 debut of Gcore’s AI public cloud service powered by NVIDIA’s H100 GPUs in Korea.

Market Segmentation

By Service

- Infrastructure as a Service (IaaS): Enables clients to rent IT infrastructure such as servers and storage on a pay-as-you-go basis, supporting scalable and flexible IT deployments.

- Platform as a Service (PaaS): Provides developers with a managed environment and tools for application development, reducing complexity and accelerating deployment timelines.

- Software as a Service (SaaS): Allows users to access software applications over the internet, eliminating installation needs and reducing costs. SaaS dominates the market as per the report.

By Workload

- Application Development and Testing: Supports businesses in building and validating applications quickly in a cloud-based environment for efficiency.

- Analytics and Reporting: Delivers real-time data analysis and business insights through cloud platforms for better decision-making.

- Data Storage and Backup: Offers secure and scalable storage options for critical business data, supporting disaster recovery strategies.

- Integration and Orchestration: Streamlines workflows by integrating multiple applications and automating processes in cloud environments.

- Resource Management: Holds the largest share and enables optimal allocation and monitoring of computing resources, supporting cost savings and regulatory compliance.

- Others: Includes additional or specialized workloads not covered in the main categories.

By Deployment Mode

- Public: Majority share; provides cloud infrastructure openly accessible via the internet, facilitating quick and affordable adoption across industries.

- Private: Ensures dedicated infrastructure for specific organizations, offering enhanced security and compliance.

- Hybrid: Combines public and private cloud benefits, supporting flexible and efficient resource usage across environments.

By Organization Size

- Large Enterprise: Largest share; these organizations need robust, resource-intensive solutions to handle complex, geographically dispersed operations.

- Small and Medium Enterprise: Smaller businesses use cloud for scalability and cost-efficiency, accessing advanced technology without extensive investment.

By Vertical

- BFSI: Largest segment; leverages cloud for analytics, risk management, CRM, and more, responding to dynamic market and compliance requirements.

- IT and Telecom: Utilizes cloud for network operations, scaling services, and managing large volumes of data effectively.

- Retail and Consumer Goods: Employs cloud platforms for omnichannel sales, customer engagement, and inventory optimization.

- Energy and Utilities: Uses cloud for real-time monitoring, resource optimization, and smart grid management.

- Healthcare: Adopts cloud for secure data sharing and healthcare IT modernization, enhancing patient outcomes and compliance.

- Media and Entertainment: Leverages cloud for content delivery, streaming, and collaborative production.

- Government and Public Sector: Implements cloud for citizen services, data management, and digital transformation.

- Others: Covers unclassified or niche segments with unique cloud needs.

By Region

- East

- West (dominant)

- Southwest

- Southeast

Ask For an Analyst- https://www.imarcgroup.com/request?type=report&id=2754&flag=C

Regional Insights

The West region of South Korea dominates the cloud computing market, attributed to its well-established IT infrastructure and concentration of major corporations and financial institutions in cities like Seoul and Incheon. The area is recognized as a hub for innovation with a highly skilled workforce and state-of-the-art data centers, supporting complex cloud services and driving regional market leadership.

Recent Developments & News

In April 2024, Gcore, a Korean AI firm, launched its first AI public cloud service in Korea, powered by NVIDIA's H100 GPUs, with 40 servers hosted in its data center. In January 2024, Korea Quantum Computing (KQC) collaborated with IBM, utilizing IBM’s AI software, infrastructure, and quantum computing services, including Watsonx. Also in January 2024, Samsung Electronics and Google Cloud established a multi-year partnership to bring generative AI technology to Samsung smartphone users in South Korea.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

Tel No: (D) +91 120 433 0800,

United States: +1-201971-6302